As February moves into its second week, financial markets are navigating a more nuanced landscape shaped by corporate earnings updates and evolving monetary policy expectations. By February 12, investors have shifted from broad early-year positioning to a more selective, data-driven approach.

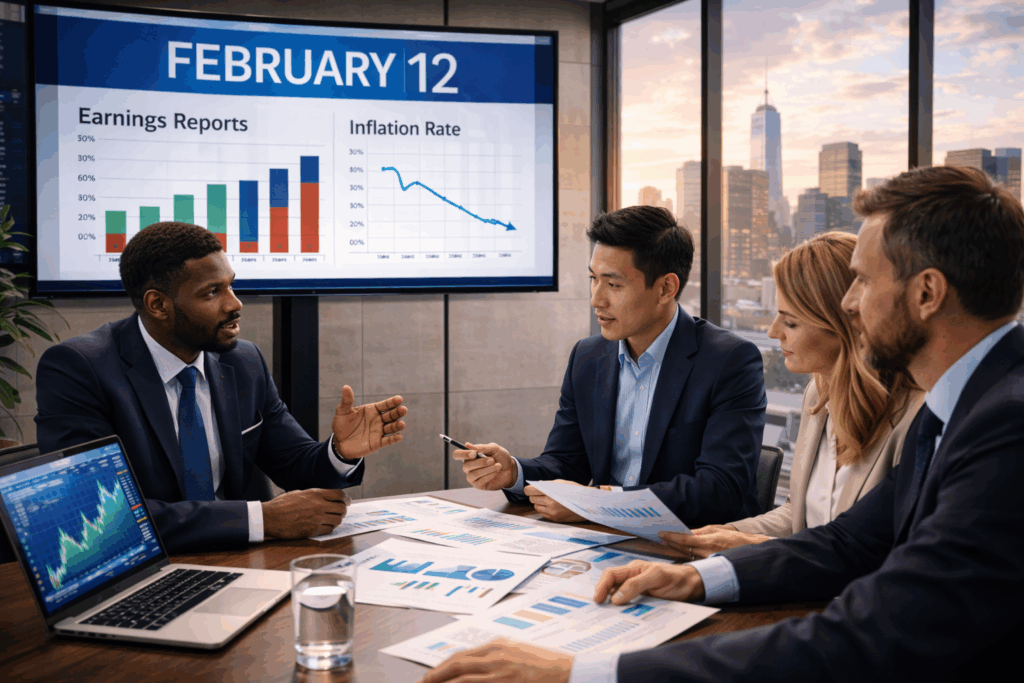

U.S. equity markets have shown resilience in recent sessions, supported by stronger-than-expected earnings from several large-cap companies. Technology, financial services, and industrial sectors have provided leadership, reflecting continued demand and operational efficiency improvements. However, investors remain attentive to forward guidance, as executives outline expectations for the remainder of 2026 amid tighter credit conditions.

Inflation data released in early February continues to reinforce the narrative of gradual moderation. While price pressures have not fully normalized, the overall trend suggests improved stability compared to the volatility of recent years. This has helped temper fears of additional aggressive rate tightening, though policymakers continue to stress a cautious and disciplined stance.

Bond markets reflect this balancing act. Yields have stabilized, signaling that investors are increasingly confident inflation risks are contained, yet remain mindful of potential surprises in upcoming economic reports. Market volatility has eased relative to January, but sentiment remains sensitive to policy commentary from major central banks.

In Europe, economic signals remain mixed. Business activity in services sectors has improved modestly, while manufacturing continues to face structural headwinds. Investment in digital infrastructure and renewable energy remains a core focus for policymakers seeking long-term competitiveness. Equity markets across the region have responded positively to improved inflation metrics, though gains remain measured.

Asian markets have benefited from improving trade flows and stabilization in manufacturing output. Regional governments continue to implement targeted stimulus measures aimed at strengthening domestic demand and supporting innovation-driven sectors. Investors are closely monitoring currency movements and global demand indicators as key variables influencing regional performance.

Corporate strategy in mid-February reflects a disciplined tone. Many firms are prioritizing cost management, balance-sheet strength, and strategic capital allocation over rapid expansion. Mergers and acquisitions activity remains selective, centered on technology integration, supply chain resilience, and productivity enhancement.

As markets approach the latter half of February, attention will increasingly turn to upcoming economic data releases and central bank communications. While uncertainty has not disappeared, the overall tone suggests a period of stabilization—one defined less by volatility and more by careful recalibration of growth expectations.